Financial stability

When does volatility become a crash?

2019-10-21 — 2017-05-15

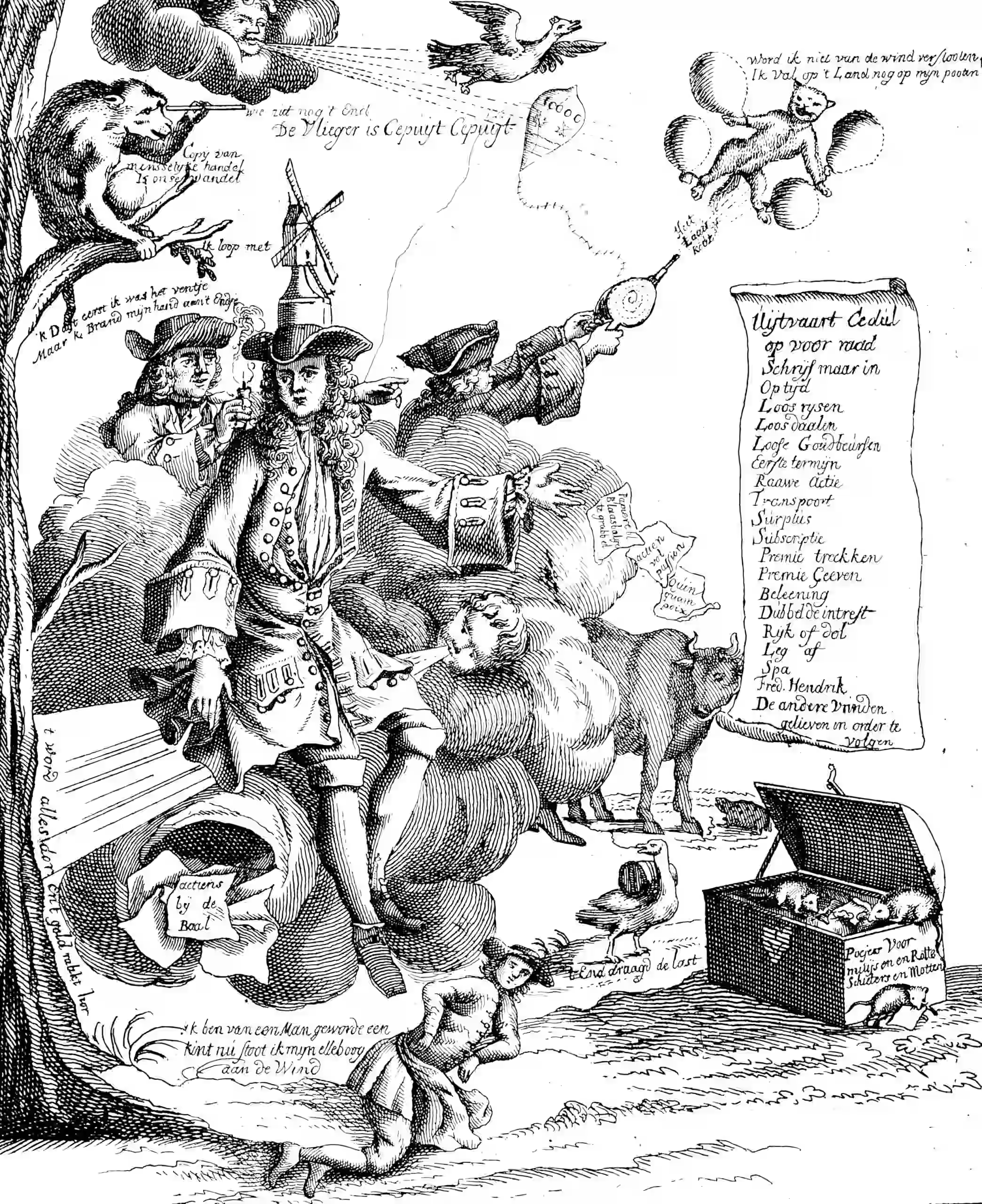

Wherein 1720 South Sea and Mississippi Speculations Are Surveyed via Satirical Dutch Engravings From Het Groote Tafereel Der Dwaasheid, and the Visual Record Is Invoked to Trace Episodes of Market Panic and Asset Bubbles.

Placeholder.

?ref=danmackinlay.name#/media/File:Het_Groote_Tafereel_der_Dwaasheid,_Wie_redeneeren_wil_is_mis,_men_vind_de_Lapis_by_de_gis.jpg){kind=link}

1 Generic financial stability

Wired’s breathlessly enthusiastic coverage of (Harmon et al. 2011).

🚧TODO🚧

2 Diversion

You know what is fun? Het Groote Tafereel der Dwaasheid, (Het Groote Tafereel Der Dwaasheid … Familien En Persoonen Van Hooge En Lage Stand Zyn Geruineerd, En in Haar Middelen Verdorven, En De Opregte Negotie Gestremt, Zo in Vrankryk, Engeland Als Nederland … Gedrukt Tot Waarschouwinge Voor De Nakomelingen in ’t Noodlottige Jaar, Voor Veel Zotte En Wyze 1720) a 1720 Dutch book about the South Sea Bubble, the Mississippi Bubble, and … is there tulip mania in there somewhere? I cannot remember, but the whole thing is online and the engravings are incredible.

- De Actiewereld op haar einde, 1720, naar Pieter Jansz. — “Speculator at the end of the world”

- Quincampoix in duigen, anoniem, 1720 — Angry speculators trashing the joint

- The South Sea Bubble, 1720 for a bit of context

- Het Groote Tafereel der Dwaasheid at Harvard

- The Great Mirror of Folly, Or Het Groote Tafereel Der Dwaasheid at Yale